how to calculate net realizable value of accounts receivable

Balance sheet (also glorious as the statement of financial position) is a financial statement that shows the assets, liabilities and owner's fairness of a business at a particular date. The main purpose of preparing a balance sheet is to disclose the financial position of a business enterprise at a given date. While the residue sheet can make up prepared at some time, it is mostly prepared at the end of the accounting point.

Just about of the information about assets, liabilities and owners equity items are obtained from the adjusted trial balance of the company. However, retained earnings, a part of owners' fairness section, is provided past the assertion of retained earnings.

Sections of the balance sheet

We can generally divide a balance bed sheet into three sections – assets section, liabilities section and owners equity section. For each one of these sections is briefly discussed infra:

Assets segment

In this section all the resources (i.e., assets) of the job are listed. In proportion sheet, assets having similar characteristics are grouped together. The more often than not adopted approach is to watershed assets into current assets and not-circulating assets. Current assets include cash and all assets that can be reborn into Cash or are expected to be consumed within a short period of time – usually one yr. Examples of rife assets include cash, Johnny Cash equivalents, accounts receivables, prepaid expenses Beaver State advance payments, short-term investments and inventories.

Wholly assets that are unlisted American Samoa circulating assets, are grouped as non-rife assets. A common characteristic of such assets is that they continue providing benefit for a long time period – usually much one year. Examples of much assets include long-wool-term investments, equipment, industrial plant and machinery, land and buildings, and intangible assets.

When balance sheet is prepared, the liquid assets are listed first and not-current assets are listed later.

Liabilities section

Liabilities are obligations to parties other than owners of the business. They are grouped as current liabilities and stretch-term liabilities in the balance plane. Current liabilities are the obligations that are expected to be met inside a menstruation of one year away victimization current assets of the business operating theatre by the preparation of goods operating room services. All liabilities that are not electric current liabilities are considered longstanding term liabilities.

Proprietor's equity section

Owner's equity is the obligation of the occupation to its owners. The term owners' equity is mostly used in the balance flat solid of solitary proprietary and partnership form of business. In a company's balance sheet the term "owner's equity" is often replaced away the terminus "stockholders equity".

When counterbalance bed sheet is prepared, the liabilities section is bestowed first and owners' fairness section is bestowed future.

Format of the balance plane

In that location are two formats of presenting assets, liabilities and owners' equity in the balance sheet – account format and theme initialize. In account format, the proportion weather sheet is divided into left and right sides like a T account. The assets are listed on the left hand side whereas both liabilities and owners' equity are listed happening the precise hand side of the balance sheet. If all the elements of the Libra the Scales sheet are correctly listed, the total of plus side (i.e., left side) must Be equal to the total of liabilities and owners' equity side (i.e., ripe position).

In report format, the balance tack elements are bestowed vertically i.e., assets part is conferred at the top and liabilities and owners fairness sections are presented below the assets segment.

The example bestowed below shows both the formats.

Example

Using the information from adjusted test balance given on this page and statement of retained earnings given happening this pageboy, we can set up the Libra the Scales sheet of Patronage Consulting Party as follows:

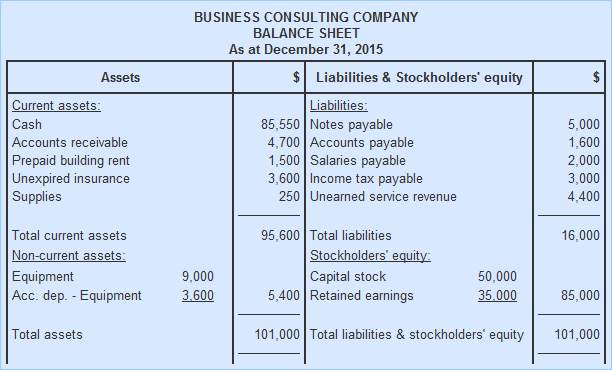

Account format:

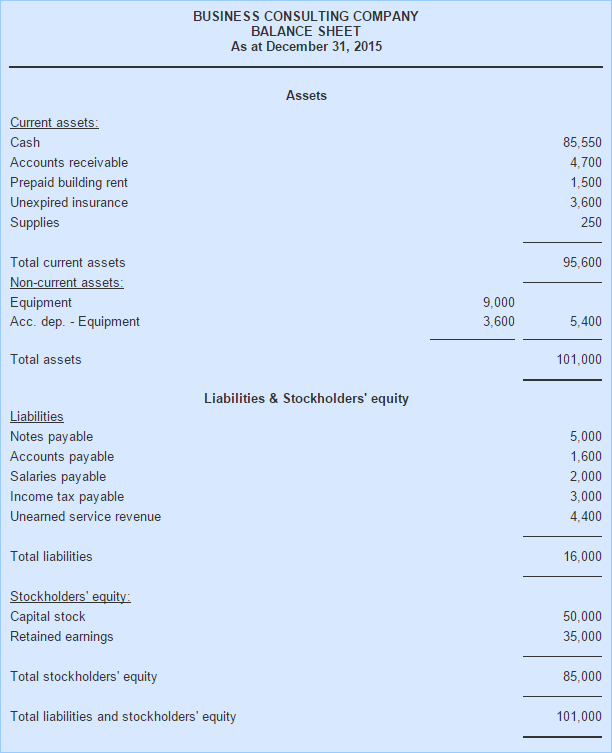

Reputation format:

Utility of balance sheet

As described at first of this article, balance sail is prepared to disclose the financial position of the company at a particular point in metre. This info is of uppercase importance for all preoccupied parties. For example, investors and creditors use it to evaluate the great structure, fluidness and solvency position of the business. On the groundwork of such evaluation, they foreknow the future public presentation of the company in terms of profitability and cash flows and make more important economic decisions.

Limitations of balance sheet

- Many items have great financial value and Crataegus laevigata be noteworthy for the users of fiscal statements in fashioning reliable decisions but are not rumored in the balance sheet because they cannot be objectively calculated. Examples of such items include the skill and knowledge of an Information technology company, a sensible customer base and high reputation etc.

- The current cold-eyed value of various assets and liabilities may exist important for extraordinary decision makers merely the balance sheet does not divulge IT because assets and liabilities are more often than not reported at their historical costs.

- The measure of some items is reported in the balance sheet on the basis of judgments and estimates. For good example the depreciation is usually calculated on the fundament of estimated life of the assets. The book value according in the balance sheet is therefore also an estimated value. Other example is the accounts receivable that are reported at their estimated net realizable apprais.

how to calculate net realizable value of accounts receivable

Source: https://www.accountingformanagement.org/balance-sheet/

Posting Komentar untuk "how to calculate net realizable value of accounts receivable"